As we head into 2024, there are some important changes to retirement limits that you should be aware of. Staying informed about these changes is crucial to ensuring your savings plan remains strategically on track with your retirement goals. So, let’s dive into the key updates.

401(k), 403(b), 457 Plans, and Thrift Savings Plan

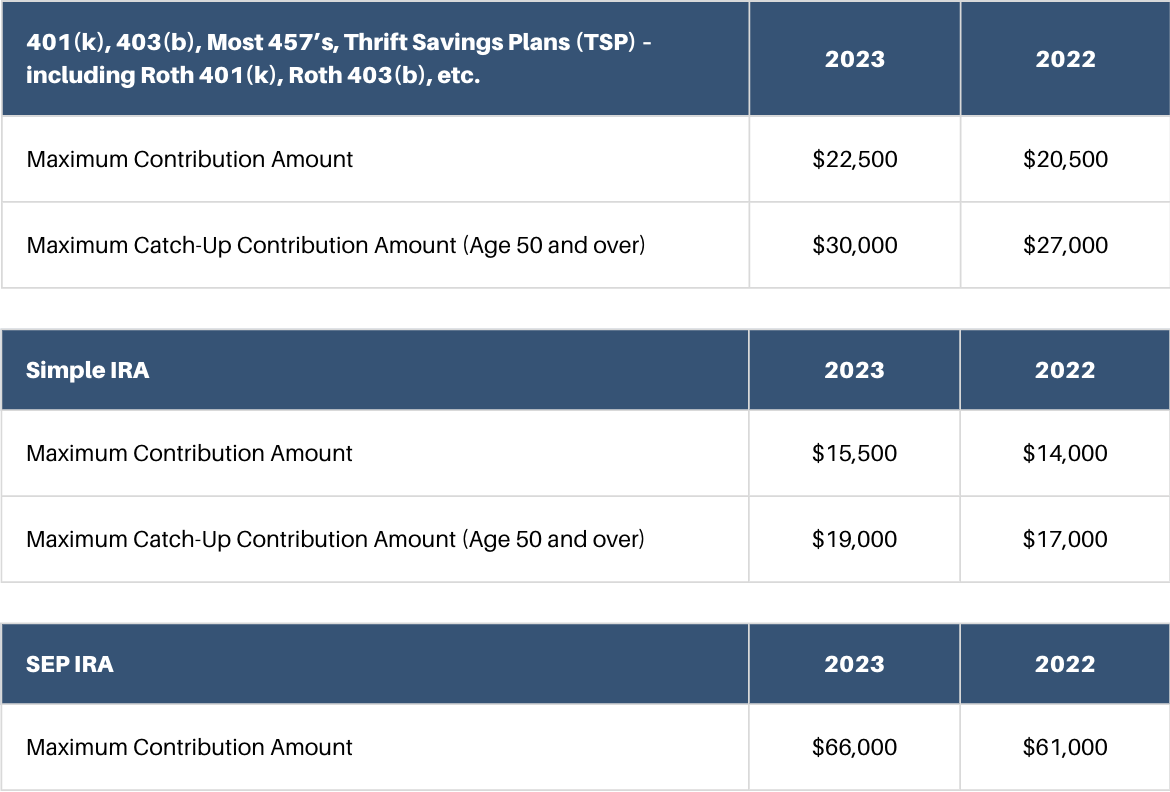

For those of you contributing to employer-sponsored retirement plans, the contribution limit has increased to $23,000 for 2024. That’s a slight rise from the previous year’s limit of $22,500.

If you’re aged 50 or older, you can still make catch-up contributions, and this limit remains at $7,500. This catch-up provision allows older individuals to contribute more to their retirement accounts, bringing the maximum contribution for 2024 to $30,500.

Traditional and Roth IRAs

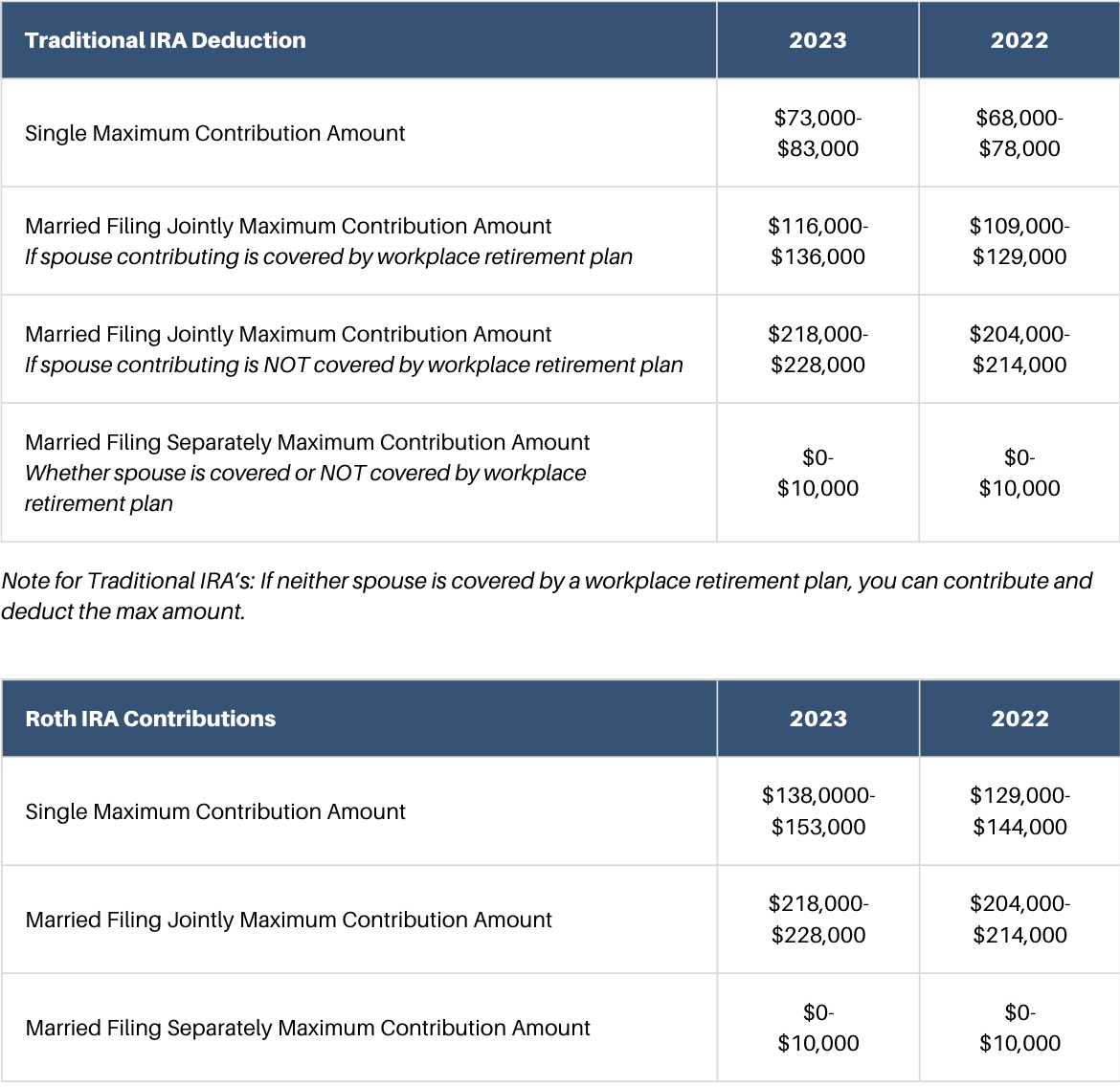

If you have a Traditional or Roth IRA, the annual contribution limit has been raised to $7,000 for 2024, up from $6,500 in 2023. This increase allows you to save even more for your retirement.

Just like with employer-sponsored plans, if you’re 50 or older, you can take advantage of a catch-up contribution. This allows you to contribute an additional $1,000, bringing your total contribution limit to $8,000.

Income Phase-Out Range for Roth IRAs

Another important change to note is the modification in the income phase-out range for Roth IRA contributors. For single filers and heads of household, the range is now between $146,000 and $161,000. If you’re married and filing jointly, the updated range is between $230,000 and $240,000.

As we enter 2024, we encourage you to review your retirement plans considering these new limits. Ensuring that your savings align with your retirement goals is crucial for financial success in your golden years.

If you have questions or need assistance with your retirement savings strategy for 2024, don’t hesitate to reach out to our experienced team at SBC Wealth Management. We’re here to help you navigate the ever-changing landscape of retirement planning and make the best decisions for your financial future.

Remember, the key to a comfortable retirement is informed decision-making and a well-thought-out savings strategy. Start your 2024 financial planning on the right foot by staying informed and taking proactive steps towards securing your retirement.

Here’s to a successful and prosperous retirement journey in the year ahead!