As of Friday, July 16th, the S&P 500 Index, with dividends reinvested, has returned a robust 16.12% to start the year. This comes on the heels of a 17.4% total return for the index for all of 2020. Interestingly, if you measure the index’s performance from last year’s market bottom on March 23rd through the end July 16th, the index is up 97.61%. In other words, the S&P 500 has nearly doubled in a little more than a year. Who would have guessed that would be the case as we were on the brink last March?

Bonds on the other hand, as measured by the Bloomberg Barclays US Aggregate Bond Index, have not fared as well in 2021. As of July 16th, the index was down -0.94% year-to-date. Although, this is much improved from the end of the 1st quarter of 2021 when the index was down -3.39% for the year. Since 1980, this index has only finished negative 3 times for a calendar year (1994, 1999 and 2013).1

What has powered these moves?

For stocks, it has been the hope and eventual realization of the re-opening of our economy. As vaccinations rose and cases, especially deaths, plummeted, people decided it was time to get out of the house and start doing normal activities again. Air travel, hotel stays, gasoline usage is all higher than one year ago. Corporate earnings have rebounded in a way that no one expected with expectations for full year 2021 earnings that are 20% above those from calendar year 2019.

For core bonds, whose prices move inversely to interest rates, it has been an up and down year thus far. We started the year with a yield on the 10-year US treasury note at 0.92% and it rose all the way to 1.75% on March 31st – a negative for bond prices. Since April 1st, the 10-year yield has slowly fallen back below 1.2% as of July 19th – a positive for bond prices but not enough to recover the losses from the first quarter.

What could impact the rest of the year?

Looking forward, we have identified a couple topics we believe has the potential to impact returns through the end of the year and beyond. Those are the trajectory of inflation and continued stimulus from the Federal Reserve and Congress.

Inflation has been leading the headlines lately and for good reason. The year over year increase in June for the Consumer Price Index (CPI), which is the most common measure of inflation in the U.S., came in at 5.4%.2 This is the largest 12-month increase since August 2007-2008. While this sounds frightening and harkens many back to the runaway inflation of the 1970’s, a look under the hood at the drivers of recent inflation reveal some interesting details which lead us to believe that headline inflation figures will likely moderate over the next 6-12 months.

The first of these details comes from the course we have been on since this time last year. Prices for gasoline, hotel rooms and airfares were in the cellar a year ago, but as we have steadily reopened as a country, these prices have naturally come back. This has been referred to as “base effects” by commentators. In other words, these prices started from an unnaturally low base during the pandemic only to rebound back to more normal prices a year later. For reference, gasoline is up 45.1%, airline fares up 24.6% and hotel and motel room rates are up 16.9% over the last year. We expect these forces to moderate as the economy normalizes.2

The second issue comes from supply shortages that have come about because of the massive supply chain disruptions that have occurred over the last 12 months. The prime example of this phenomenon has played out in the used vehicle market. A shortage of microchips used in manufacturing new vehicles has caused scarcity in the availability of these cars and trucks. As a result, the overall demand for vehicles and limited supply of vehicles has caused prices to rise. Used car and truck prices increased 10.5% in June alone and accounted for more than one third of the monthly CPI increase.2 Like the impact from “base effects,” we expect this trend to moderate as the supply chain for vehicles comes back online.

When we look at other important components of CPI such as food (+2.4% year over year) and rent of primary residence (+1.9% year over year), we are encouraged that the situation is not as dire as it may seem in the headlines.

Of course, there are risks though. Right now, the market is pricing in an annual rate of inflation of about 2.41% over the next 5 years which seems reasonable.3 But if some of these short-term price increases last longer than expected and higher prices are eventually passed on to consumers, it could stifle spending. If this occurs, economic growth could potentially stall which would increase the chances of recession.

Monetary policy, or more simply Federal Reserve policy, with the monthly purchase of $120 billion of Treasury bonds and mortgage-backed securities (MBS) that began at the start of the pandemic, has flooded the market with cash. This has helped keep both stock markets afloat and short-term interest rates near zero. But as the market heats up, we expect the Fed to begin slowing or “tapering” their purchases of Treasuries and MBS to prevent the economy from potentially overheating. We do not expect the Fed to begin tapering in 2021 but we do expect conversations and comments from the Fed around the timing of tapering to begin in the latter half of the year. When and whether they act will all come down to the rate of GDP growth, the rate of inflation and the health of the labor market as we close out 2021.

Fiscal policy, on the other hand, has the potential to be a wild card. As we sit here today, there is a potentially $1 trillion infrastructure spending package that is nearing bipartisan agreement. If passed, this infrastructure package would possibly supplement a much larger, $3.5 trillion spending and tax credit plan with only Democratic party support. With the larger bill focusing on “antipoverty, education and climate” comes the likelihood of higher corporate taxes and capital gains taxes for those making over $400,000 per year to off-set the massive spending. Negotiations have been going on for months and it may be months more before anything gets settled, if at all.

The primary concern, if both bills pass, could likely be that the additional government spending, on top of an already churning economy, would have the ability to stoke already simmering inflation by introducing more cash into the hands of consumers. Additionally, a hike in corporate taxes would have an almost immediate negative impact on the value of most corporations and their stock prices.

There is also the possibility that none of these bills get passed or, at least not until sometime next year. I would say that the market is currently pricing a high likelihood of these bills or some similar variation passing through Congress, but if those expectations change and uncertainty creeps into the market it could bring with it higher volatility in stock and bond prices.

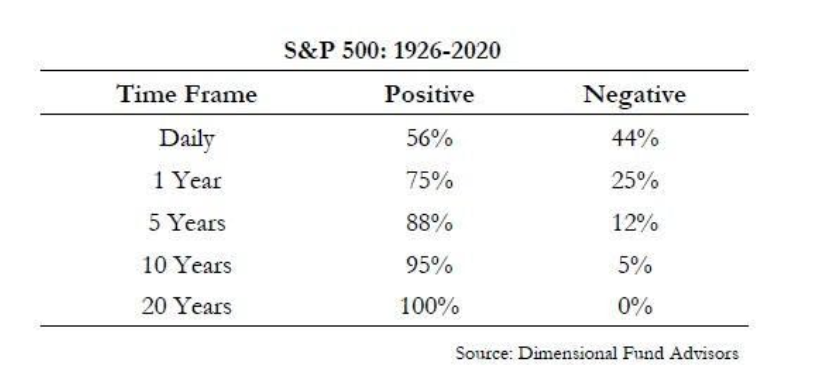

Taking all of this into account, there have always been reasons to be cautious about having your money in the market or investing new money. But markets, over the long term, have always climbed that wall of worry. Consider this, since 1926 investing in the S&P 500 for only one day at any given time you would have had a positive return 56% of the time – a little better odds than a coin flip. Investing for any one year on the other hand you would have had a positive return 75% of the time. For any 5-year period you would have positive returns 88% of the time, 95% of the time over any 10-year period and 100% of all 20-year periods.

But getting there is not easy. Within any given year you would have, on average, experienced 3 declines of more than 5% and at least one decline of 10% or more.

With these facts in mind, we at SBC construct client investment portfolios to be prepared for short-term disruptions but remain appropriately positioned to take advantage of the long-term probabilities.

Sources:

- Source: Morningstar Direct

- https://www.bls.gov/news.release/cpi.t07.htm

- https://fred.stlouisfed.org/series/T5YIE