With the S&P 500 Index down close to 16% and the US Aggregate Bond Index down almost 10% year-to-date, there has been nowhere to hide in markets. Frankly, the start to the year has been awful any way you slice it.

Whether it stems from inflation, Fed policy, the dire situation in Ukraine, the strong US Dollar or declining US economic growth, there’s plenty of uncertainty out there at the moment. We acknowledge these are trying times.

But it is moments like these that separate successful long-term investors from the rest. We believe this is when our value as advisors truly makes the most difference – helping our clients navigate rough waters.

Staying the course and sticking to a financial plan in times like these is difficult. We all know markets don’t always go up but when corrections occur it just doesn’t sit right.

Our natural instinct as human beings is to take action when we sense danger. Unfortunately, this instinct leads us to wanting to make emotional decisions about our investments at the most inopportune times. Even if doing nothing at all is the best option.

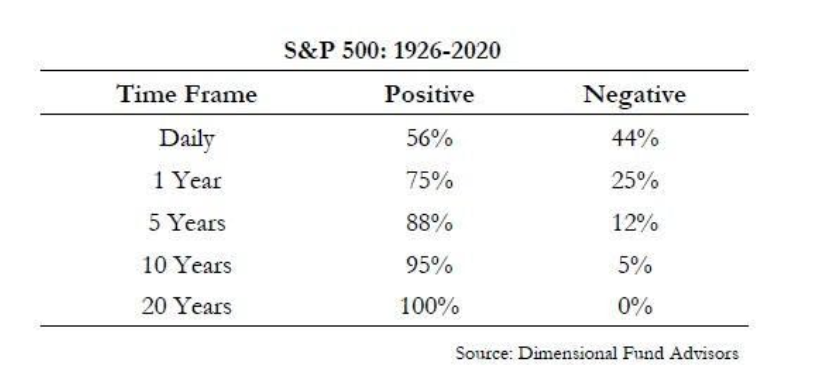

As studies have shown, investors who try to get in and out of markets at the “right time” have consistently underperformed investors that stay invested.

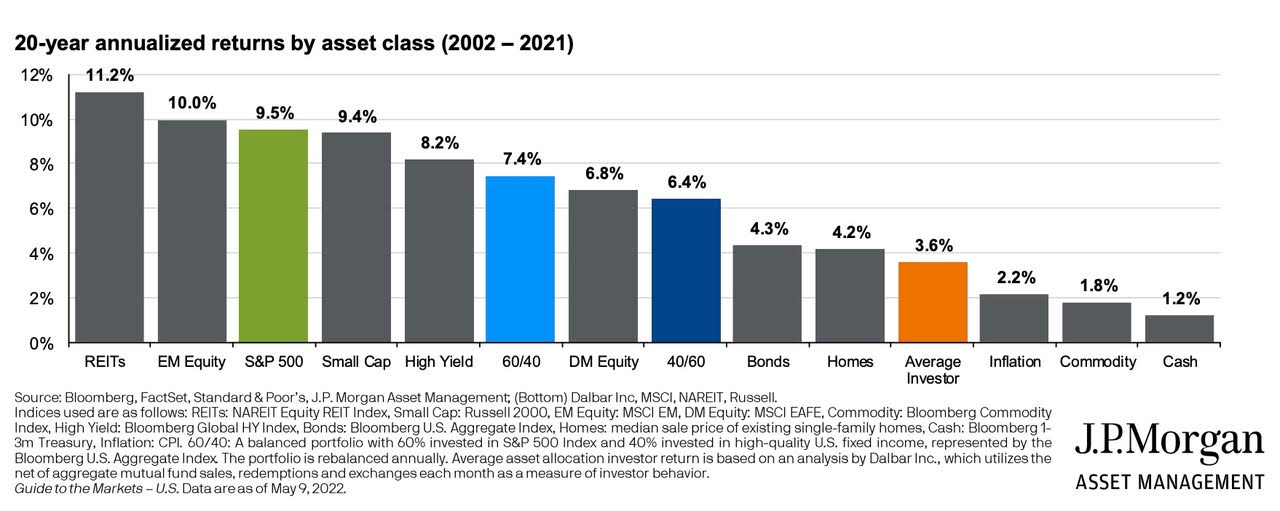

JPMorgan Asset Management reports that, from 2002 to 2021, based on research from Dalbar, Inc, the average investor had an average annual return of 3.6%. While a fully invested portfolio consisting of 60% stocks and 40% bonds returned 7.4% annually.

In other words, the average investor does not have a great track record of timing when to get in and out of the market.

As further proof that it is difficult to know when to get in or out, we only have to look back a couple of years. The S&P 500 bottomed on March 23rd, 2020, about the time the US and global economies essentially closed their doors for business due to Covid. The S&P 500 was down over 30% from its all-time high a month earlier. Things looked bleak.

But given the benefit of hindsight, we now know March 23rd, 2020 was the best day to put money into the stock market during the pandemic. It was, in fact, when things looked the worst and not when things were starting to feel better that produced the best future returns.

Here is the good news though. I know a lot of individuals and families who were fully invested on March 23rd, 2020. I know these individuals and families because they are clients of SBC Wealth Management, and they rode the bull market through the end of 2020 and again through 2021. Not because they knew the market was going to do well or felt good about the economy, but because they were sticking to a plan and had stayed invested through the good times and the bad.

So here we are again. Bad times in the markets have returned. We don’t have control over the current events causing uncertainty and we don’t know what the markets will do tomorrow.

We do, however, have control over the investment decisions we make and the plans that were created with these times in mind.

Is now the time to abandon ship? I don’t believe so.

With all that said, if you haven’t already, now could be a great time to revisit your financial plan with your SBC advisor. As always, we are determined and prepared to help you and your family through these rough waters.

The information provided in this post is being provided for educational and informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Those seeking information regarding their individual financial needs should consult a financial professional. Opinions expressed are current as of the day of posting but are subject to change without notice based upon changing market, economic, political, or social conditions. All information is from sources deemed to be reliable, but no warranty is made as to its accuracy or completeness. SBC, our employees, or our clients, may or may not be invested in any individual securities or market segments discussed in this material. Past performance is no guarantee of future results and any opinions presented can not be viewed as an indicator of future performance. Investing involves risk, including loss of principal.