There’s no such thing as a free lunch.

The phrase “free lunch” refers to a once-common tradition of saloons offering a free lunch to patrons who purchased a drink. Often the foods included at lunch were high in salt, so those who ate the free lunch would inevitably be thirsty for at least one additional drink.1

Urban legend aside, the phrase acknowledges that a person or society cannot get “something for nothing.” This certainly has been the case for stock investing in 2022. While I’m typing, we are experiencing a correction in the S&P 500 (down over 10% from the all-time high) and a bear market in the technology-heavy Nasdaq (down over 20% from the all-time high).

While these bumps in the road may feel tough to stomach while they’re happening, periods of negative performance are not all that uncommon for the stock market historically. In fact, since 1950, the S&P 500 has experienced 36 corrections, 10 bear markets, and 6 crashes. This translates to a correction (-10%) roughly every 2 years, a bear market (-20%) every 7 years, and a crash (-30%) every 12 years.2

This is precisely why our investment philosophy centers around building diversified portfolios that are durable in all market environments. In the past, stock market volatility has historically provided opportunities to rebalance and buy stocks “on sale” using proceeds from bond investments (buy low, sell high).

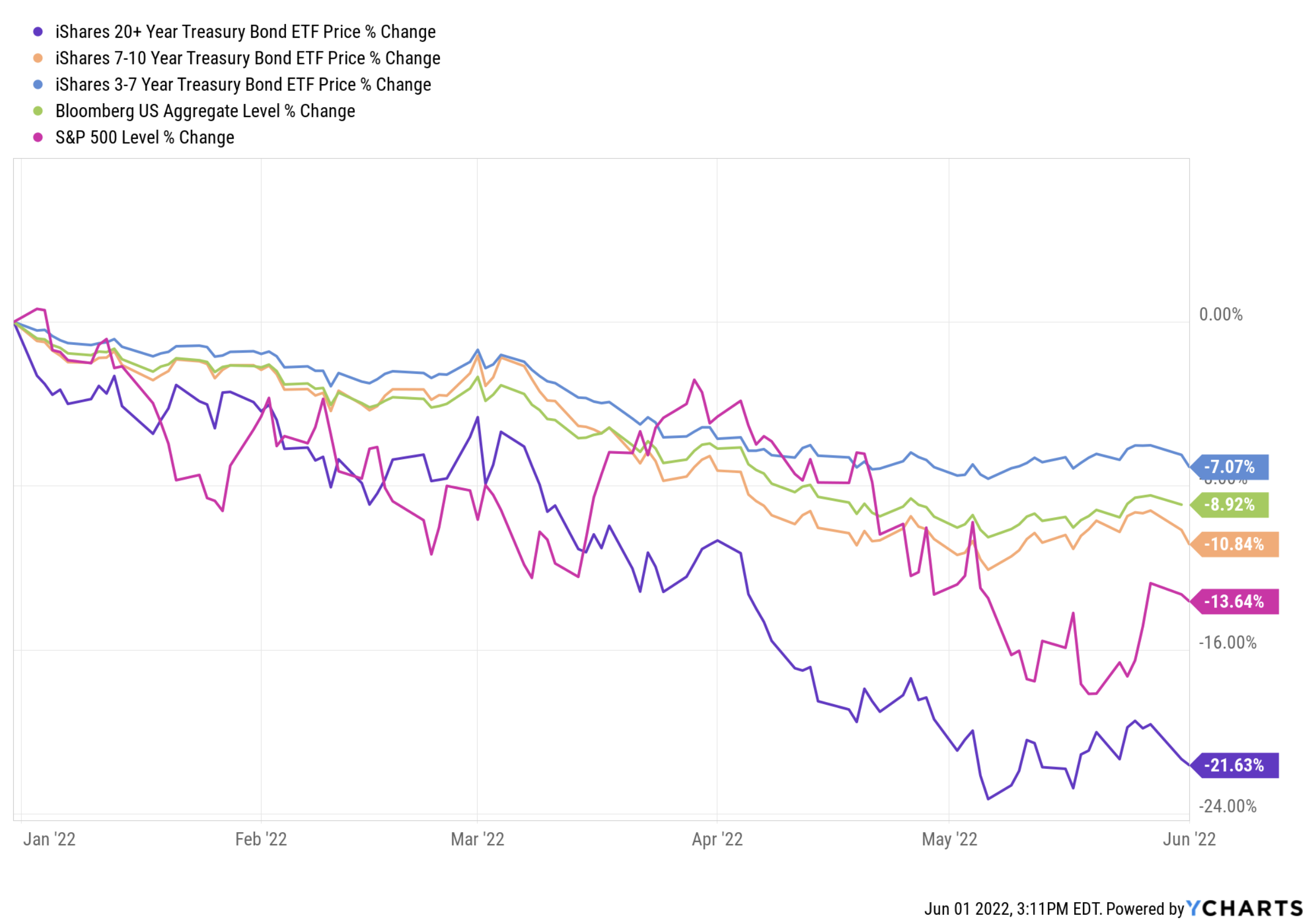

What has made 2022 uniquely challenging, however, has been the severe negative performance of US Bonds:

A combination of restrictive monetary policy, rising interest rates, and inflation have created a “perfect storm” for bond investors resulting in their worst quarter of performance in over 40 years.3

In response, economists, PhD’s and market pundits have begun to question whether bonds should have a role in your portfolio. Clients with an aggressive risk tolerance, or those planning to build wealth for future generations are wondering, “Why would I invest in bonds making 3% per year when inflation is running over 8%? Why not just invest 100% in stocks?” Indeed, locking in a negative 5% inflation-adjusted (real) return on your bond investments doesn’t sound great, but this way of thinking ignores why we choose to invest in bonds in the first place:

“We buy stocks so we can eat well, but we buy bonds so we can sleep well.” – Cliff Asness4

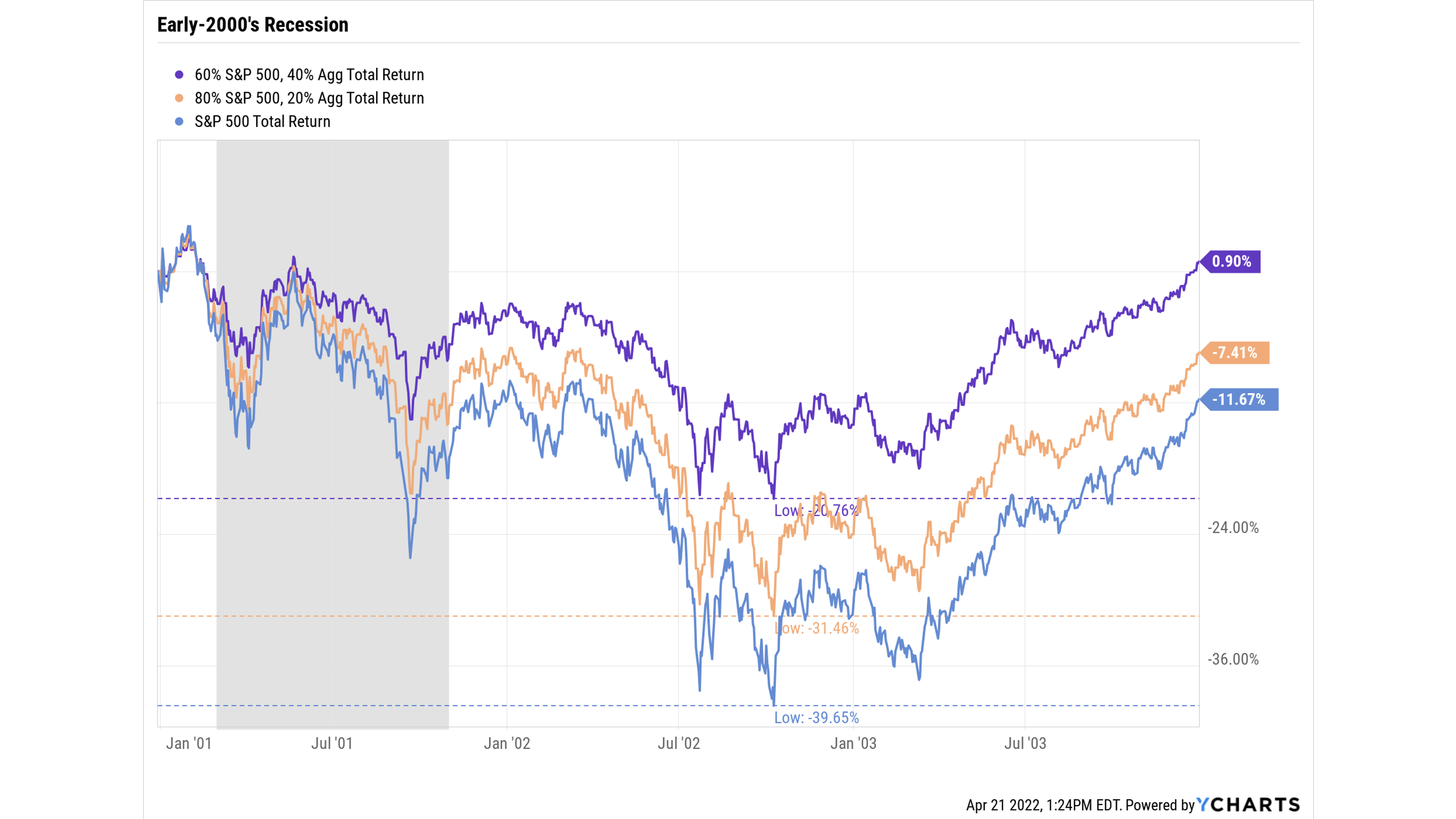

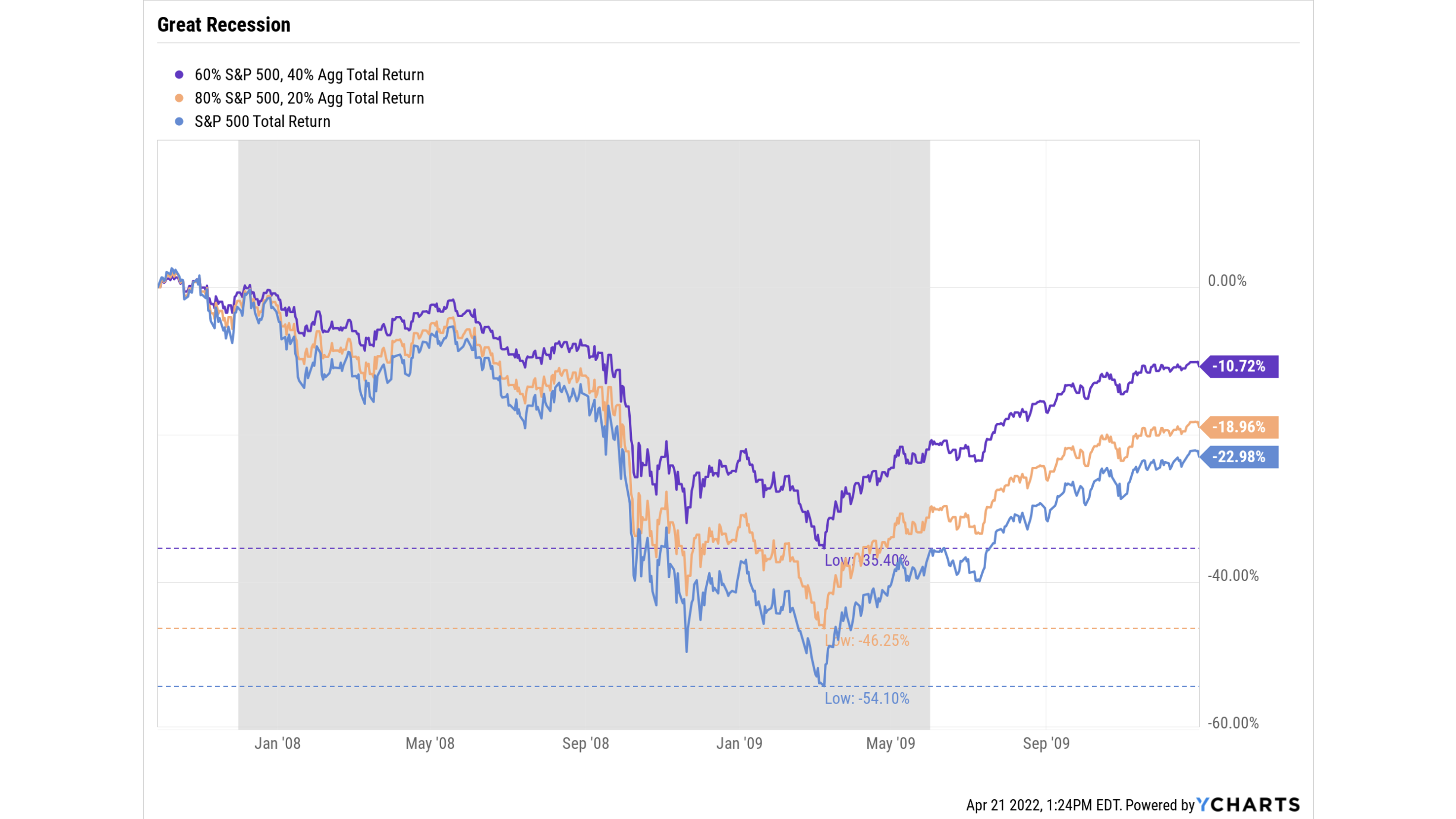

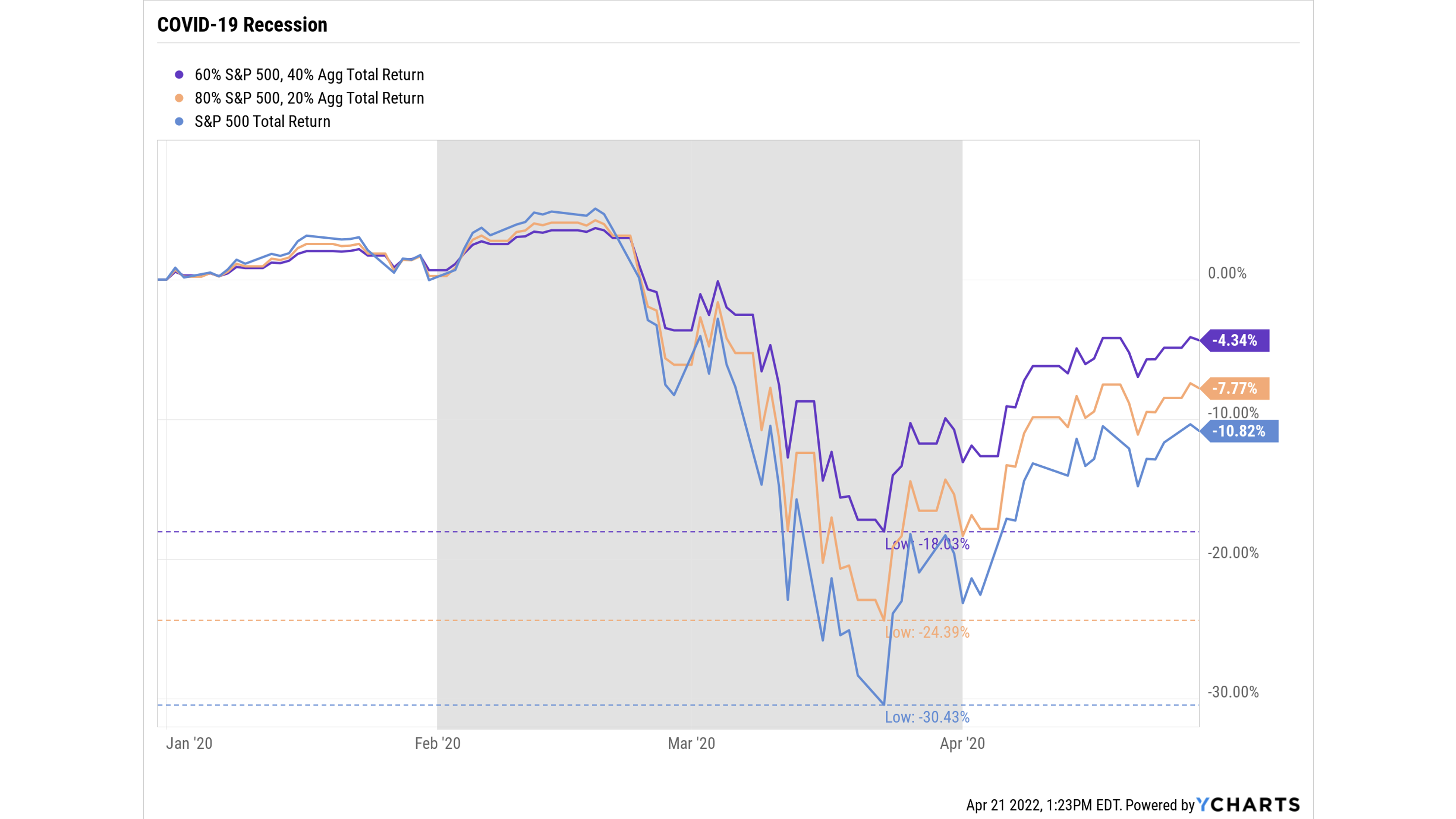

Bond investments generally provide a consistent income stream and greater safety of principal. If your portfolio is a boat, then picture your bond investments are your ballast. When winds, waves, and other forces of nature threaten to tip or capsize your boat, your ballast allows it to maintain its balance and power through. During market crashes, demand for bonds tends to surge, as investors exchange risky assets for safer investments in what’s commonly called a “flight to safety.” This is why portfolios with more bonds in them have experienced less of a crash in the past three recessions:

More importantly, investors that owned bond investments and rebalanced during the above crashes experienced an even bigger benefit during the recovery that followed. Of course, correctly timing the rebalancing would have required some luck but having that ability and owning bonds in the first place didn’t happen by chance.

Retirees and folks nearing retirement age know that negative returns are much more painful later in life. So, while the talking heads sell fear of recession and aim to convince the public that there is no alternative to stocks (“TINA”), remember bonds will be your safety net for the next black swan event. Removing our emotions and taking our lumps can be difficult in the short-term for even the most intelligent investors. This is why it’s important to maintain a long-term, rules-based investment philosophy and why it pays to have professional help.

The information provided in this post is being provided for educational and informational purposes only and should not be considered an individualized recommendation or personalized investment advice. Those seeking information regarding their individual financial needs should consult a financial professional. Opinions expressed are current as of the day of posting but are subject to change without notice based upon changing market, economic, political, or social conditions. All information is from sources deemed to be reliable, but no warranty is made as to its accuracy or completeness. SBC, our employees, or our clients, may or may not be invested in any individual securities or market segments discussed in this material. Past performance is no guarantee of future results and any opinions presented can not be viewed as an indicator of future performance. Investing involves risk, including loss of principal.

Sources:

- https://en.wikipedia.org/wiki/There_ain%27t_no_such_thing_as_a_free_lunch

- https://awealthofcommonsense.com/2022/01/how-often-should-you-expect-a-stock-market-correction/#:~:text=Over%20this%2072%20year%20period,every%207%20years%20(20%25%2B)

- https://www.wsj.com/articles/fed-signals-half-percentage-point-increases-could-be-warranted-at-coming-meetings-11649268002?mod=article_inline

- Maggiulli, Nick. Just Keep Buying. HARRIMAN HOUSE PUBLISHING, 2022.

- Economic and Market Commentary | Advisor Perspective from Kevin Sasena, MBA, SBC Wealth Advisor

- Breaking Market Commentary | May 2022 from Andrew Fairman, CFA, CFP(R), SBC Wealth CIO